A $524 million storage reservoir project in Labelle provided a significant boost to overall national construction starts statistics in June, according to a report from Dodge Data & Analyi. The river/harbor development category provided the lift, rising 164% in June.

The vast majority of work will be done by C-43 Water Management Builders Joint Venture, which provided the South Florida Water Management District (SFWMD) with the lowest bid, News-Press.com has reported. The companies participating in the joint venture are Salini Impregilo and Lane Construction.

A local publication, the Lake Okeechobee News, reported earlier that SFMD officials were making efforts to ensure opportunities for smaller contractors and suppliers to obtain work related the massive project.

“Back in May, we had an ‘Industry Day,'” SFWMD project chief Thomas McKernan told Hendry County commissioners in January. “We wanted anybody interested in bidding this project to come out, see the site and the size and magnitude of this project, but we also wanted them to be introduced to some of the local guys who work out here that know the area.

“We met in West Palm Beach, gave a big presentation, and the following day we came out and drove the site, let these guys talk to each other, hand out cards and started dialogue between some of the local guys and some of the bigger firms,” McKernan explained.

He went on to state that although the prime contractor will be a large company — “it has to be, to bond a job of this size — but there’s also an SBE requirement that they’ll be required to take on local, smaller firms as well. We also prequalified those contractors, ended up with six, on the four major features — the dam being the primary one, the soil/bentonite cutoff wall, the soil-cement lining and the structures. We didn’t want these guys coming out, this being their first rodeo, so we made sure they were prequalified on jobs of this size and scope.”

Nationally, overall construction starts in June advanced 9% from the previous month to a seasonally adjusted annual rate of $832.7 billion, according to Dodge. The increase followed the 10% gain reported for May, as total construction starts continued to strengthen following April’s subdued performance.

By major sector, much of the lift in June came from a 16% jump for nonresidential building, which reflected the start of the $1.1 billion expansion to Terminal 5 at Chicago’s O’Hare International Airport, as well as sharp gains for office buildings, public buildings (detention facilities and courthouses), healthcare facilities, and warehouses. The other two major sectors registered moderate growth in June, with nonbuilding construction up 6% and residential building up 5%. Through the first six months of 2019, total construction starts on an unadjusted basis were $378.8 billion, down 8% from the same period a year ago. On a 12-month moving total basis, total construction starts for the 12 months ending June 2019 were 4% below the amount for the twelve months ending June 2018.

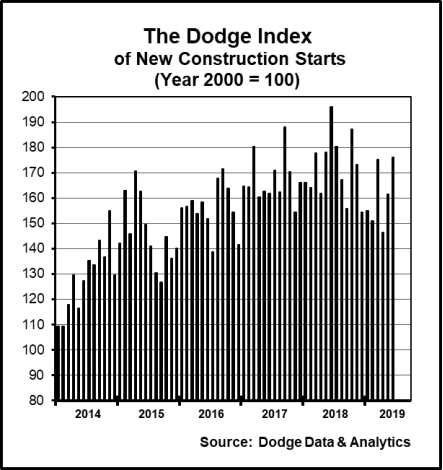

June’s data raised the Dodge Index to 176 (2000=100), compared to an upwardly revised 161 for May. June’s reading was the highest so far for the Dodge Index during 2019, topping the 175 for March, and coming in slightly above the full year 2018 average for the Dodge Index at 172. On a quarterly basis (which helps to lessen the volatility present in the monthly data), the Dodge Index edged up 1% during the second quarter of 2019, helped by the improved activity in May and June after a weak April. This followed a 7% decline during this year’s first quarter compared to the final three months of 2018.

“On balance, the pace of construction starts has been sluggish so far in 2019, as activity has been generally lower than the healthy amount reported during the first half of 2018,” said Robert A. Murray, chief economist for Dodge Data & Analytics. “The improved activity during May and June suggests that the gap relative to last year should narrow in coming months.”

“Several features of the first half of 2019 stand out, as shown by the construction start statistics,” Murray saod. “For nonresidential building, the commercial and institutional building segments have stayed close to their 2018 amounts, but manufacturing plant construction has not seen the same number of very large projects that were reported last year. For nonbuilding construction, electric utility starts have witnessed renewed growth after several years of decline, but public works construction was generally lackluster in early 2019 and the dollar amount of new pipeline projects is down considerably from last year.

For residential building, single family housing remains generally flat, adversely affected by affordability constraints. In addition, multifamily housing has lost momentum following its 2018 rebound, yet the occasional strong month like June suggests that this year’s multifamily pullback is likely to stay moderate.”

Nonresidential building in June was $308.3 billion (annual rate), up 16% which followed an 8% increase in May. The institutional building categories as a group soared 37% in June, helped in particular by a 348% jump for new transportation terminal starts. Leading the way for transportation terminal projects was the $1.1 billion expansion of Terminal 5 at Chicago’s O’Hare International Airport that was entered as a June construction start. In addition, the latest month included the $370 million Terminal E modernization project at Boston’s Logan International Airport, a $98 million terminal renovation project at San Francisco International Airport, and a $75 million terminal renovation project at Dallas-Ft. Worth International Airport. The public buildings category also had a strong June, advancing 242% as the result of these large projects – the $320 million Wayne County Criminal Justice Center in Detroit MI, the $280 million Community Justice Campus in Indianapolis IN, and a $163 million courthouse in Austin TX.

Healthcare facilities climbed 22% in June, featuring the start of six hospital projects valued each at $100 million or more that were led by the $305 million Altru Hospital in Grand Forks ND and the $245 million University of North Carolina Hospital Surgical Tower in Chapel Hill NC. Educational facilities, the largest institutional building category, edged up 1% in June as it registered growth for the third straight month. There were four high school buildings valued each at $100 million or more that reached groundbreaking in June, located in Richmond TX ($158 million), Wilkes-Barre PA ($137 million), Ames IA ($137 million), and Falls Church VA ($108 million). The top five states in terms of the dollar amount of educational facility projects that reached the construction start stage during the first half of 2019 were – Texas. California, New York, Massachusetts, and Ohio. Decreased activity in June was reported for amusement-related projects, down 7%; and religious buildings, down 43%.

The commercial side of nonresidential building increased 12% in June. The office building category advanced 31%, boosted by the start of these large data centers – the $418 million Microsoft data center in Cumming IA, a $280 million data center in Papillion NE, and a $258 million data center in Manassas VA. Other large office projects that reached groundbreaking in June were the $260 million AmerisourceBergen headquarters in Conshohocken PA, the $230 million office portion of the $300 million Avocet Tower in Bethesda MD, and the $197 million office portion of the $330 million Gateway to Minneapolis building in Minneapolis MN. Through the first six months of 2019, the top five metropolitan areas in terms of the dollar amount of new office construction starts were – Washington DC, New York NY, Boston MA, Atlanta GA, and Austin TX. Metropolitan areas ranked 6 through 10 were – Dallas-Ft. Worth TX, Richmond VA, Chicago IL, Houston TX, and Philadelphia PA.

Warehouse construction starts in June climbed 19%, boosted by the start of the $750 million Amazon Prime Air Hub at Cincinnati/Northern Kentucky International Airport, a $130 million Dollar Tree distribution center in the Houston TX area, and a $100 million Shugart Farms distribution center in Palmetto GA. The other commercial building categories experienced decreased activity in June – stores, down 1%; commercial garages, down 9%; and hotels, down 11%. Despite the decline, the hotel category did include the $86 million hotel portion of the Gateway to Minneapolis mixed-use building. Manufacturing plant construction in June retreated 45% from its robust May amount, which was boosted by the $1.6 billion Shintech polyvinyl chloride manufacturing facility in Plaquemine LA and a $600 million steel mill expansion in Osceola AR. The largest manufacturing plant projects that were entered as June construction starts were a $500 million lithium battery manufacturing plant in Commerce GA and a $250 million segment of the Foxconn LCD display manufacturing complex in Mount Pleasant WI.

Nonbuilding construction in June was $206.2 billion (annual rate), up 6% which followed a 32% surge in May. The electric utility/gas plant category continued to see strong activity, advancing 14%. Providing the lift in June was the $1.1 billion Energy Vision 2020 upgrades to wind power facilities in the states of Washington, Wyoming, and Oregon. Also contributing were two substantial projects in Wyoming – a $1.0 billion expansion to a wind power complex and a $500 million transmission line project. The public works categories as a group grew 2% in June after a 1% decline in May.

The river/harbor development category provided the lift, rising 164% in June that reflected the start of a $524 million storage reservoir in Labelle FL, a $243 million dredging project in Massena NY, and a $100 million waterfront development project in Staten Island NY. The other two environmental public works categories weakened in June, with water supply construction down 3% and sewer construction down 30%. The miscellaneous public works category settled back 4% in June after its 17% increase in May. Even with its June decline, the miscellaneous public works category did include a $789 million segment of the border wall located in New Mexico. Highway and bridge construction in June retreated 5%, settling back for the second month in a row after improved activity in March and April. The top five states in terms of the dollar amount of highway and bridge construction starts during the first six months of 2019 were – Texas, California, Florida, New York, and Illinois.

Residential building in June was $318.2 billion (annual rate), up 5% which followed a 2% gain in May. Multifamily housing registered its strongest amount since last November, advancing 26% in June. The pace for multifamily housing in June was 3% above its average monthly pace during 2018. There were 14 multifamily projects valued each at $100 million or more that reached groundbreaking in June, compared to 8 such projects in May. The largest multifamily projects in June were the following – a $640 million

multifamily building in Brooklyn NY that’s part of the Pacific Park development, a $364 million multifamily building in Jersey City NJ, and a $200 million multifamily building in Houston TX. Through the first half of 2019, the top five metropolitan areas ranked by the dollar amount of multifamily starts were – New York NY, Washington DC, Los Angeles CA, Miami FL, and Chicago IL. Metropolitan areas ranked 6 through 10 were – Boston MA, San Francisco CA, Dallas-Ft. Worth TX, Atlanta GA, and Austin TX. Single family housing in June slipped 3%, receding after a 2% gain in May, as this project type has yet to see any sustained growth during the first half of 2019. The pace for single family housing in June was 6% below its average monthly pace during 2018. By region, the first half of 2019 showed this performance for single family housing compared to last year – the South Atlantic, down 5%; the South Central, down 6%; the West, down 8%; the Midwest, down 11%; and the Northeast, down 12%.

The 8% slide for total construction starts on an unadjusted basis during the first six months of 2019 was due to reduced activity by each of the three main construction sectors. Nonresidential building fell 10% year-to-date, with this pattern by segment – commercial building down 1%, institutional building down 7%, and manufacturing building down 49%. The steep drop for manufacturing building is the result of the comparison to a very strong first half of 2018, that included such projects as a $6.5 billion uranium processing facility in Oak Ridge TN. If the manufacturing building category is excluded, nonresidential building year-to-date would be down 4%. Residential building year-to-date dropped 9%, with single family housing down 7% and multifamily housing down 14%. Nonbuilding construction year-to-date decreased 5%, reflecting a 138% jump for electric utilities/gas plants combined with a 20% decline for public works.

The miscellaneous public works category plunged 47% year-to-date, due to a sharply lower volume of new pipeline starts. If the miscellaneous public works category is excluded, public works construction during the first half of 2019 would have fallen a more moderate 6% and nonbuilding construction would be up 13%. By major region, total construction starts during the first six months of 2019 showed this behavior – the Midwest, down 5%; the Northeast, down 7%; the South Central, down 8%; and the West and South Atlantic, each down 10%.

On the basis of twelve-month moving totals, in this case the twelve months ending June 2019 compared to the twelve months ending June 2018, total construction starts were down 4% from the previous period. By major sector, nonresidential building fell 4%, with commercial building up 5%, institutional building down 6%, and manufacturing building down 28%. Nonbuilding construction dropped 7%, with electric utilities/gas plants up 42% and public works down 14%. Residential building slipped 2%, with 2% declines for both single family and multifamily housing.

{kind=link}